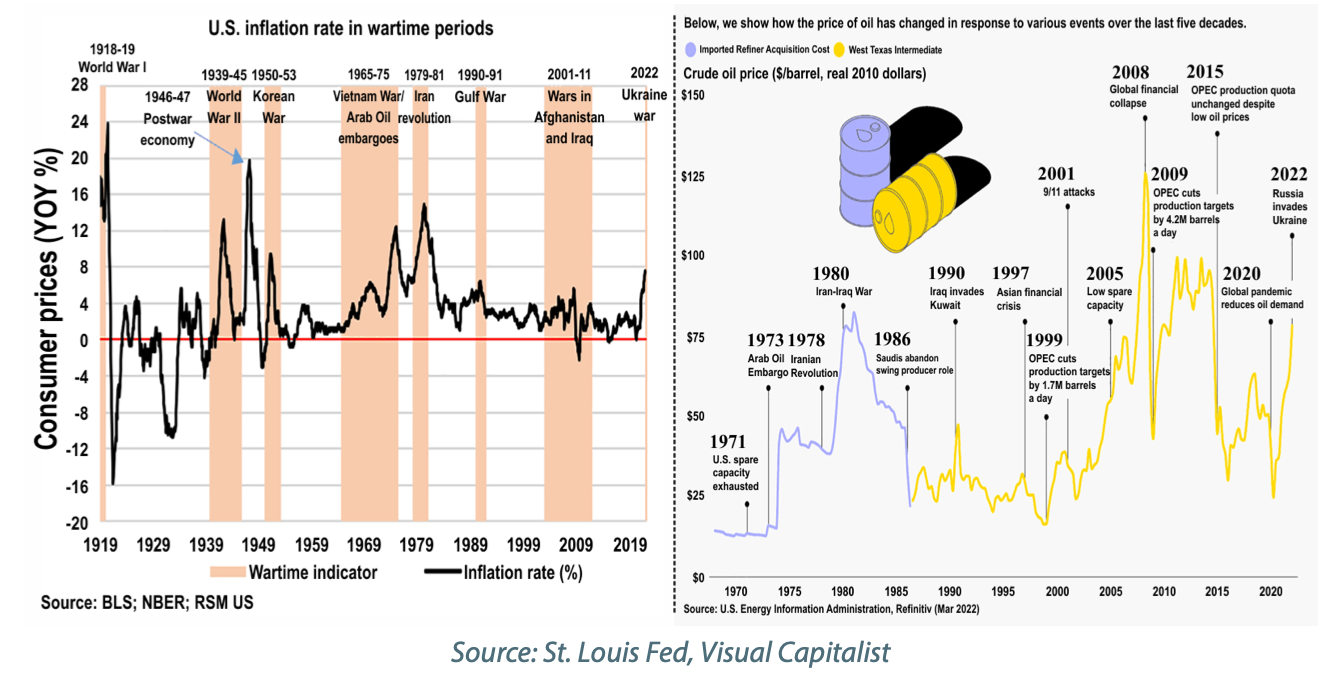

Historically, war and inflation go hand-in-hand. Demand for resources increases to build weapons and materiel, and fiscal and monetary policy are loosened to fund defence spending.

**1. Oil

Market participants are dangerously complacent in their expectation that oil prices will simply drop back down once the current hostilities are over.

-

the cycle of retaliation among this war’s participants is a “Pandora’s box” that cannot be easily closed

-

While more than 20% of global crude oil passes through the Strait of Hormuz, regional producers account for over 30% of global crude-oil production.

-

Over 75% of the world’s spare crude-oil capacity resides in just four countries in the Persian Gulf region: Saudi Arabia, the UAE, Kuwait and Iraq. And while that excess has edged downward after OPEC began hiking its output, even this overstates what is truly accessible and sustainable, because Saudi Arabia has long maintained an “iron reserve” of 1.5-2.0 million bpd. over the past several years due to fears about “stranded assets.”

-

The most reliable and accessible spare capacity this year is probably around 2 million bpd or so—equivalent to 2% or less of global consumption. This is a dangerously-low level, especially considering the recent increase in unplanned production outages. Even during the GFC output curtailment in 2009, excess capacity was over 5% of global consumption.

-

Iraq has announced meaningful production curtailments at its Rumaila and West Qurna 2 oilfields, which are among the world’s largest, because the closure of the Strait of Hormuz is causing storage facilities to fill-up too rapidly. While Washington has announced that the U.S. Navy will escort ships through the Strait, it will take time to execute. Meanwhile, there are a multitude of major oil and gas installations that could be subject to attack in the coming weeks.

-

In the unlikely event that a popular uprising takes place in Iran, or if U.S. ground forces are sent in, there will be an increased risk that Tehran will undertake a “scorched earth” policy by attacking its own energy infrastructure. Recall that the post-Saddam insurgency in Iraq wreaked havoc on energy infrastructure and hindered the recovery of production.

2. Inflationary Pressures

-

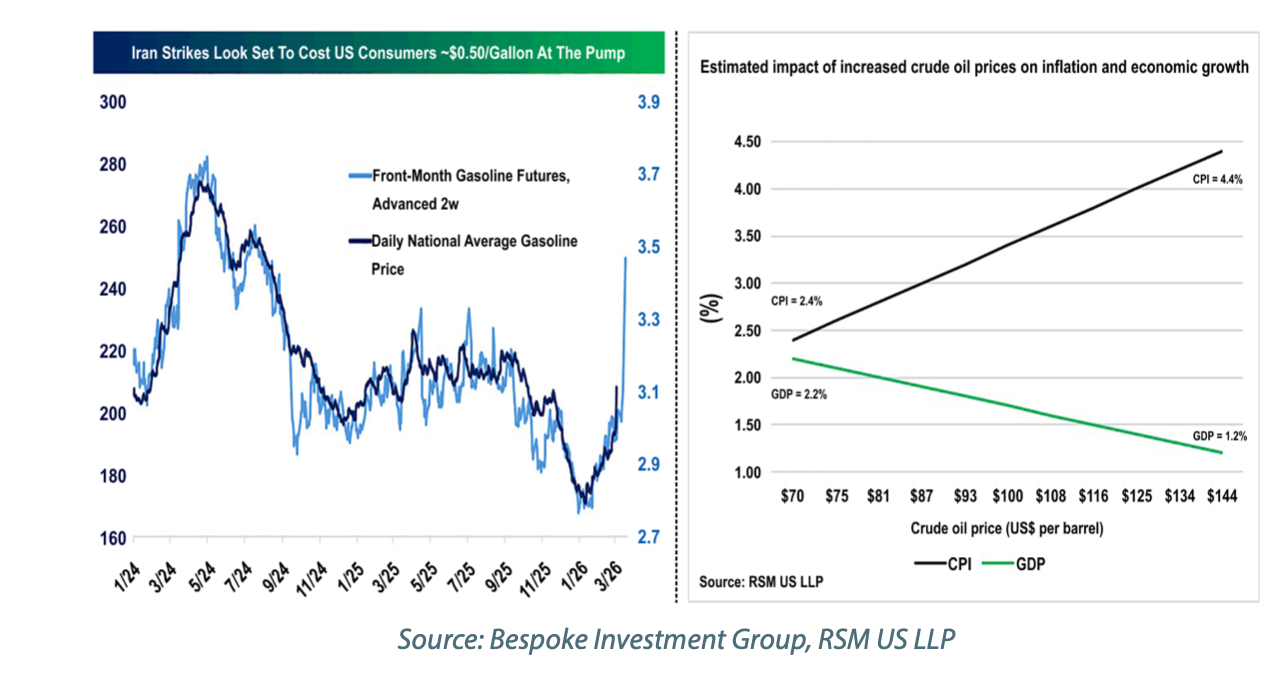

The price of crude oil has an outsized influence on the CPI because of its impact on transportation, in addition to petrochemicals and other goods. Since last April, crude oil has had a mostly negative y/y impact on the CPI.

-

WTI is now over 17% above its year-ago level, so the inflationary impact will be positive going forward. Consequently, U.S. consumers are facing a gasoline price increase of more than $0.50 per gallon over the past month.

-

Qatar, which accounts for almost 20% of global LNG exports, shut down its Ras Laffan plant, the world’s largest LNG-export facility. As a result, European natural gas futures have risen over 50% since last Friday. And, the cost of insuring a ship traveling through the Strait has spiked twelve-fold, even after Washington’s backstop offer

-

UST yields are rising instead of falling, which they normally do during times of geopolitical crisis. This price action begs the question of whether the U.S. is gradually losing its safe-haven status due to a loss of trust in Washington and the potential for higher inflation.

-

Economic models suggest that a doubling of oil prices could cause CPI inflation to nearly double while cutting GDP growth nearly in half.

-

Multiple inflation metrics are flashing warning signs:

-

The core PCE price index hit 3% in December, rising from 2.8% in October.

-

The core PPI index reached nearly 3.6% in January, up from 2.9% last August.

-

The ISM Prices Paid Index spiked to 70.5 in February, up from 59, marking its highest level since June 2022.

-