The TL;DR

- Energy Re-rating: A structural shift valuing energy as “critical infrastructure” rather than a commodity; driven by Nuclear/AI growth and Oil & Gas capex.

- The Debasement Trade: Weak USD to continue and “The Big Print” for the Fed; Central Banks and China aggressively buy Gold to de-risk from US (Treasuries and USD).

- US Economic Divergence - the K-shaped economy: “Wall St vs. Main St” gap widens; S&P 500 hits ATHs while the real economy is struggling.

- European Defence: Spending is structural, not cyclical; driven by US disengagement and a desperate need from Germany to replace crumbling industrial sectors.

- Ukraine Ceasefire: Trump pushes a “Reverse Nixon” deal to fracture Russia-China ties, likely forcing a settlement that favors Russia.

- US-China “Frenemies”: A shift to transactional cooperation; tariffs may drop in exchange for purchase commitments despite the rhetoric of the past year.

- Europe is doomed: Political paralysis and deindustrialization fuel right-wing populism, threatening EU “solidarity” with diverging interests and fiscal maths just don’t add up

- China Upside: Economy successfully pivots from property to “New Three” (EVs, Batteries, Renewables), likely beating low growth expectations.

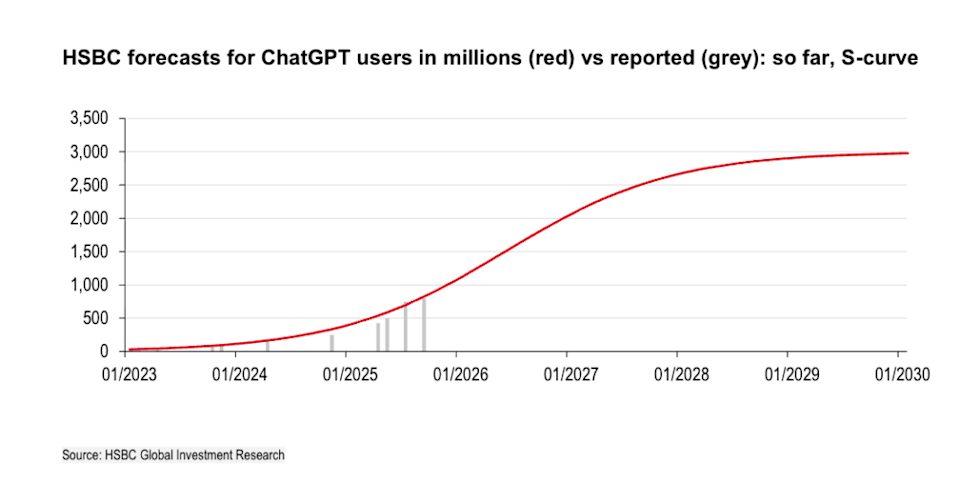

- AI Bubble: Valuations are stretched and the “Mag 7” trade fractures but the bubble must keep going until it doesn’t.

- Oil Market: Consensus points to a $60 oil. That’s the most likely case at least for 2026. A few things could challenge that narrative.

1. Energy Re-rating trade

A. Nuclear & AI (The “Growth” Re-rating - longer term)

AI is at the same time an overhyped and an under-hyped technology. The bubble exists (more of that below), but that doesn’t mean it is not a revolutionary technology that will affect almost every industry.

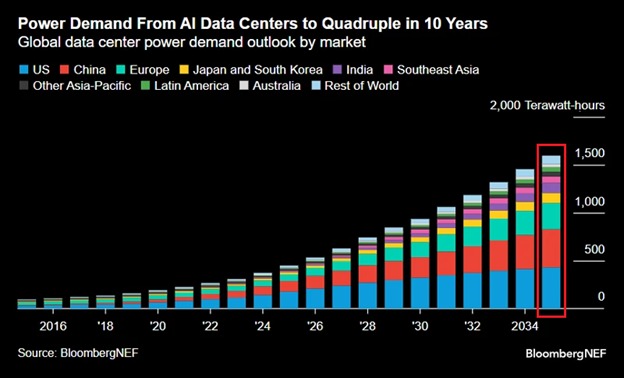

Data centres are set to consume 1,600 terawatt-hours of power demand by 2035, equal to 4.4% of global electricity.

In other words, power demand from AI data centres is set to QUADRUPLE over the next 10 years.

In major US markets, data center power demand is growing faster than that of electric vehicles, hydrogen, and other emerging technologies.

AI’s bottleneck is not chips, it’s energy.

Uranium miners, SMR builders, utilities with nuclear fleets are going to benefit.

(Even the UK! Is waking up on nuclear)

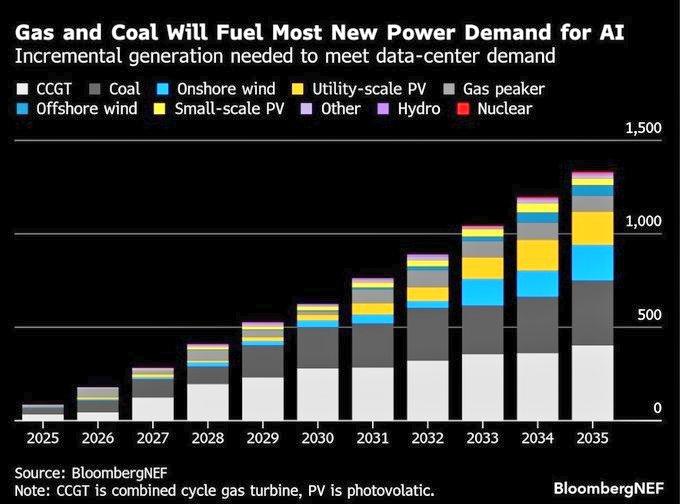

B. Oil & Gas (The “Value” Re-rating - the here and now)

Continuing from section A, Nuclear is great but it is years away when we need energy now. What we know best is.. Gas & Coal.

Energy security is one thing but combined with “capital discipline”, energy companies are poised to rip the benefits here. Instead of chasing growth and crashing prices, companies are using record profits for buybacks and dividends.

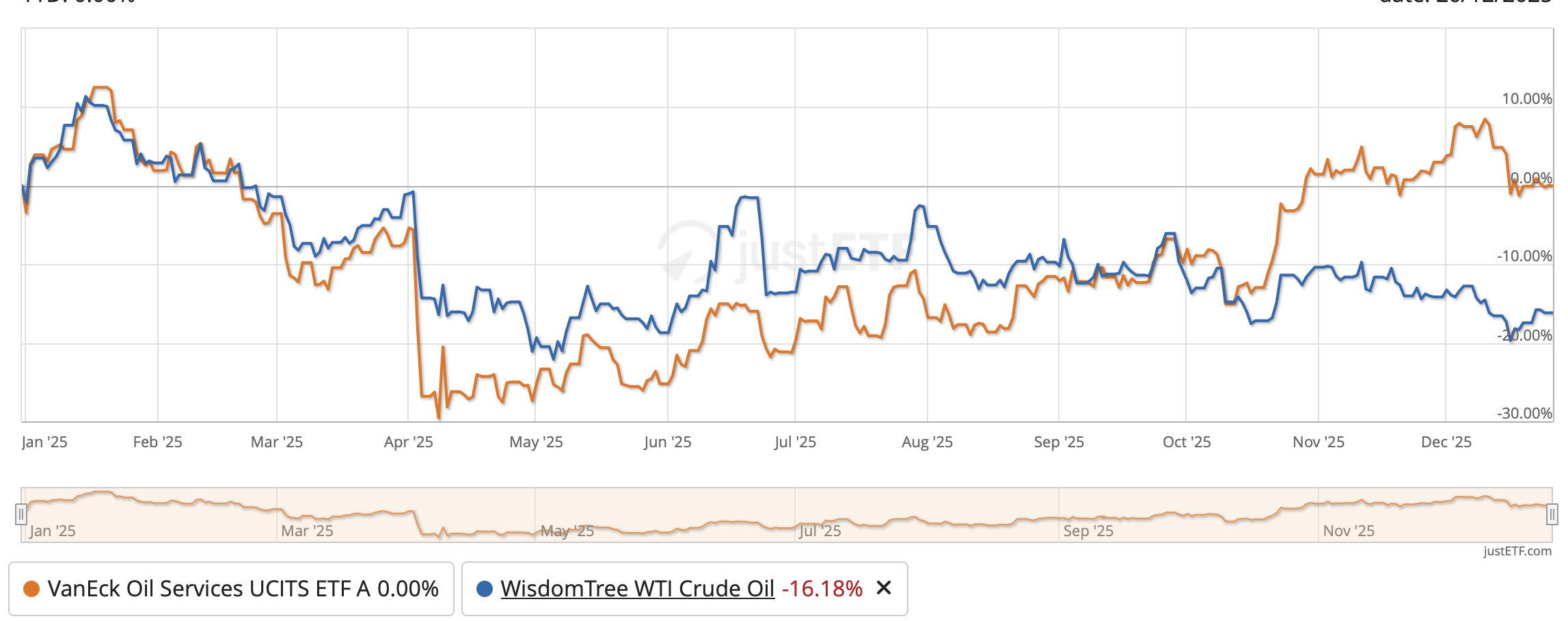

This is a chart of WTI vs OIH (energy producers). The market is pricing these companies (major oil companies and upstream/ midstream producers) from “dying industries” to “cash flow machines” that will remain profitable for decades.

At the same time capital is flowing to established energy because:

- High interest rates made capex for renewables expensive

- ESG being essentially dead in the water everywhere apart from maybe Europe

- Geopolitical instability

2. The Debasement trade and weak USD

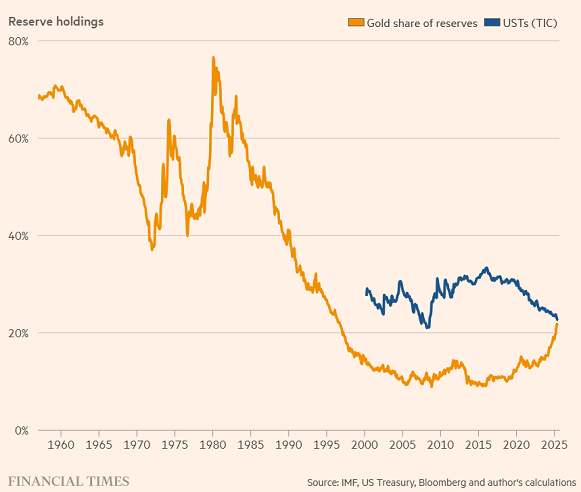

A. Geopolitical Diversification & De-dollarization: The weaponization of the US dollar via sanctions (freezing of Russian assets) has accelerated the secular trend of reserve diversification among China and the broader BRICS bloc. To mitigate sovereign sanction risk, these nations are increasingly pivoting away from Treasuries toward alternative settlement mechanisms and hard assets, specifically Gold (and they are price insensitive buyers).

B. US midterms & the Fed

Midterms in the US this year and Trump on a certain course to lose. However, he’ll try everything to avoid it. He doesn’t have a huge amount of options though.

The bond market won’t tolerate a blowout in deficit spending—yields are already too high.

Trump’s only lever is monetary. With a dovish Fed Chair (Hassett?) to force aggressive cuts, even with the S&P sitting at near ATH. It’s party time!

Even with JPOW, the Fed was quite dovish yesterday, imagine with Trump’s guy soon..

Bring out the printing press (but don’t call it QE!):

The Housing market: Trump wants to cut mortgage rates, even introduced 50-year mortgages; seen from middle-income America, this is making life more affordable - another argument for aggressive Fed cuts.

What is amazing is that this will be spun off like Trump is helping “main street” while lower rates are basically pure fuel for asset prices.

My personal favorite: The GENIUS act

(truly a scam GENIUS act). The US doesn’t need to rely on the Fed to buy Treasuries - it created a massive, price insensitive buyer of US debt.

The stablecoin companies (e.g. Tether) need to keep their token 1:1 pegged to the USD. In order to do that they hold collateral - the safest, most liquid Treasuries (T-Bills). How do they make money? Users give the issuer cash (in USD) to get a token. The issuer takes that cash and buys T-Bills to earn the yield (currently ~4-5%). They keep the interest as profit.

The GENIUS act legitimized this by mandating these companies to hold short-term Treasuries. This forces the entire crypto ecosystem to become a structural buyer of US debt.

What’s in it for the US:

i. New Buyer of Last Resort: As China and the BRICS sell Treasuries (de-dollarization), stablecoins step in to buy them.

v. USD Dominance: It entrenches the USD as the settlement layer for the digital economy. Even if you trade crypto, you are effectively trading US debt.

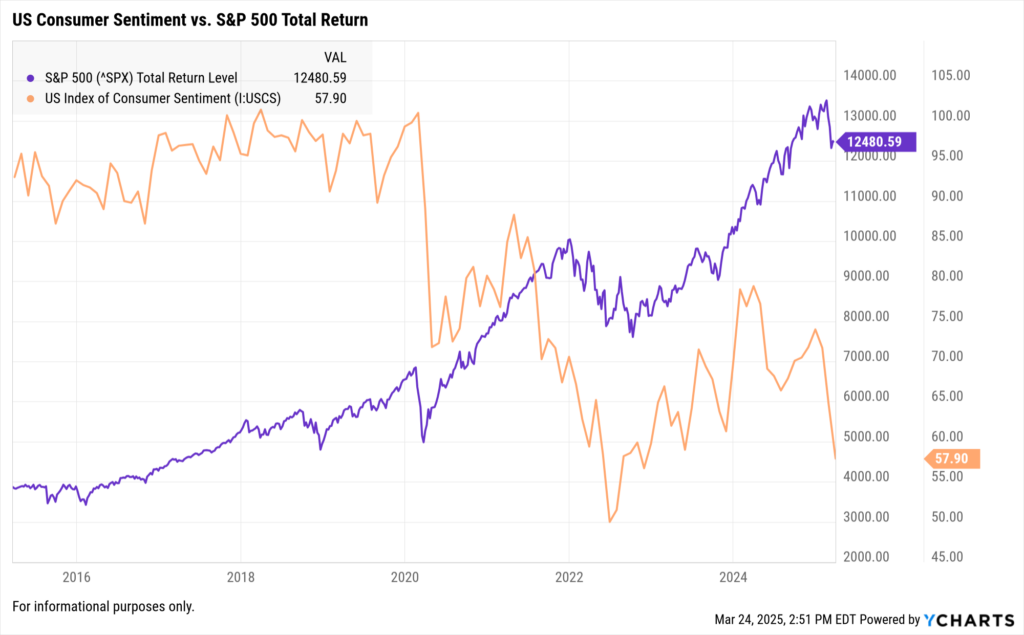

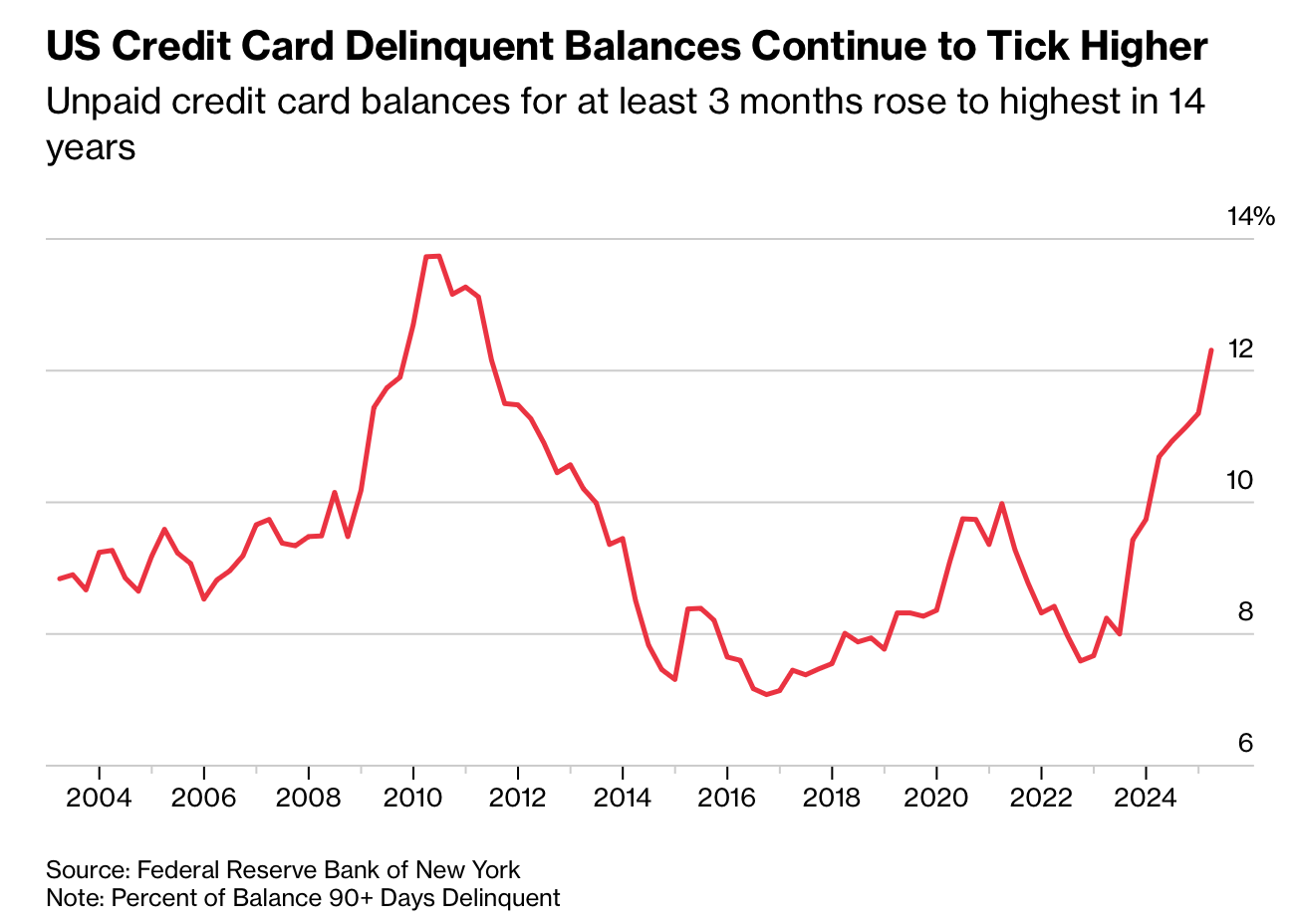

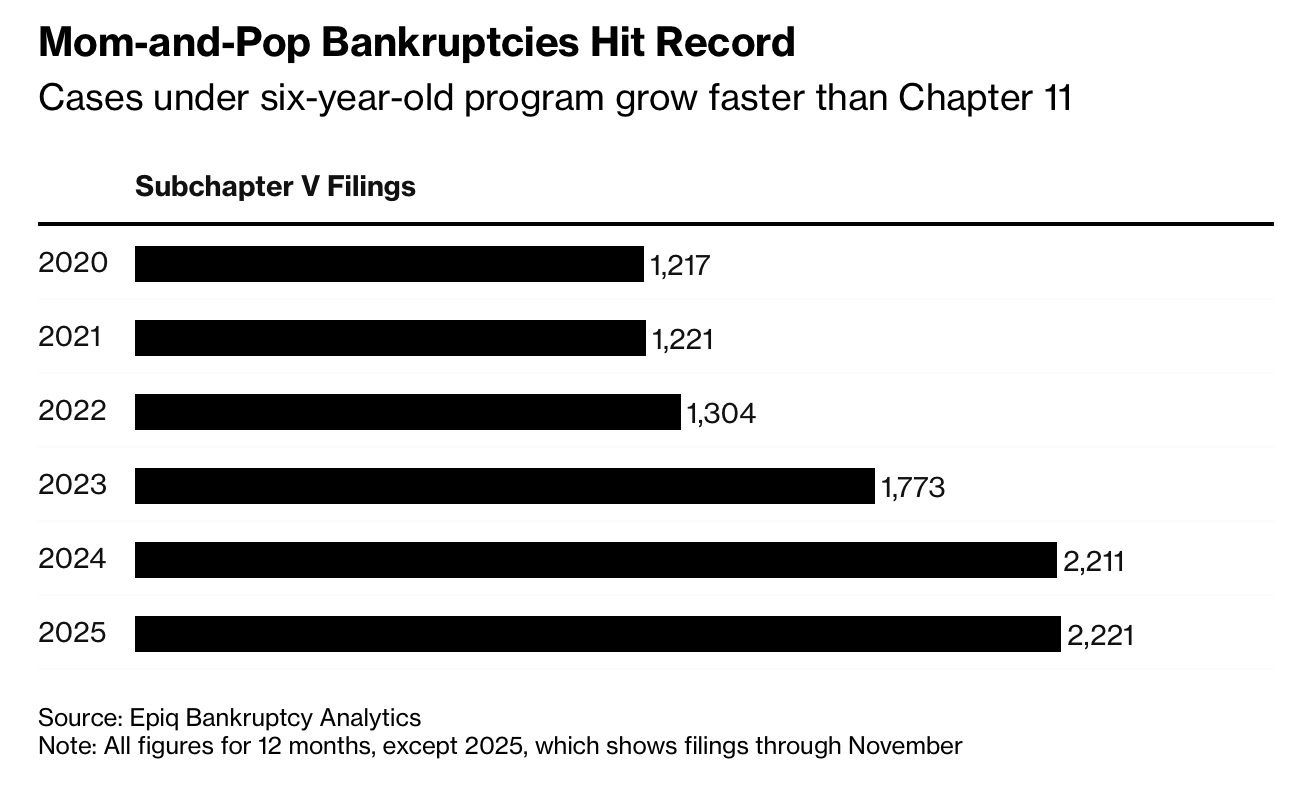

3. US Economic Divergence, Wall St vs Main St - The K-shaped economy

S&P 500 hits records while the real economy fractures.

a. Consumer Stress: Credit card delinquencies (90+ days) have surged to ~12%, the highest level in 14 years. Consumer sentiment remains depressed (index at ~51) despite the market rally.

b. Small Business Crisis: Mom-and-Pop bankruptcies have hit a record

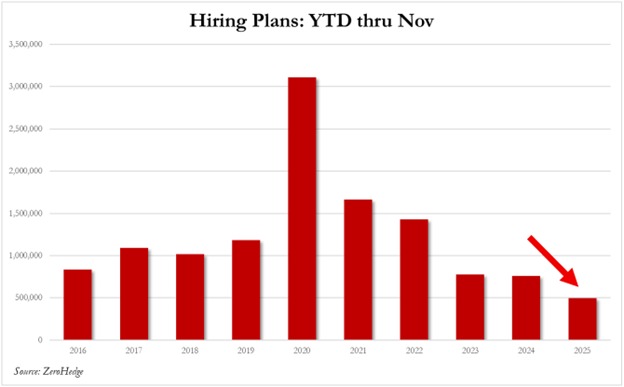

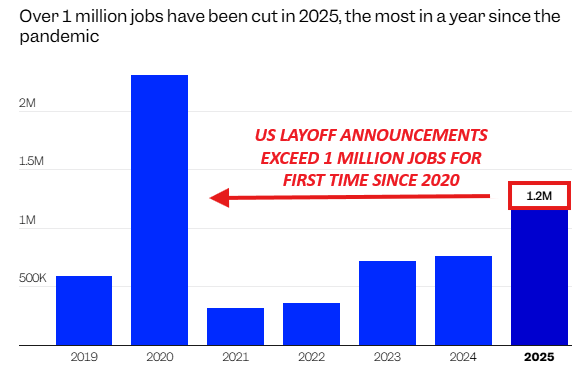

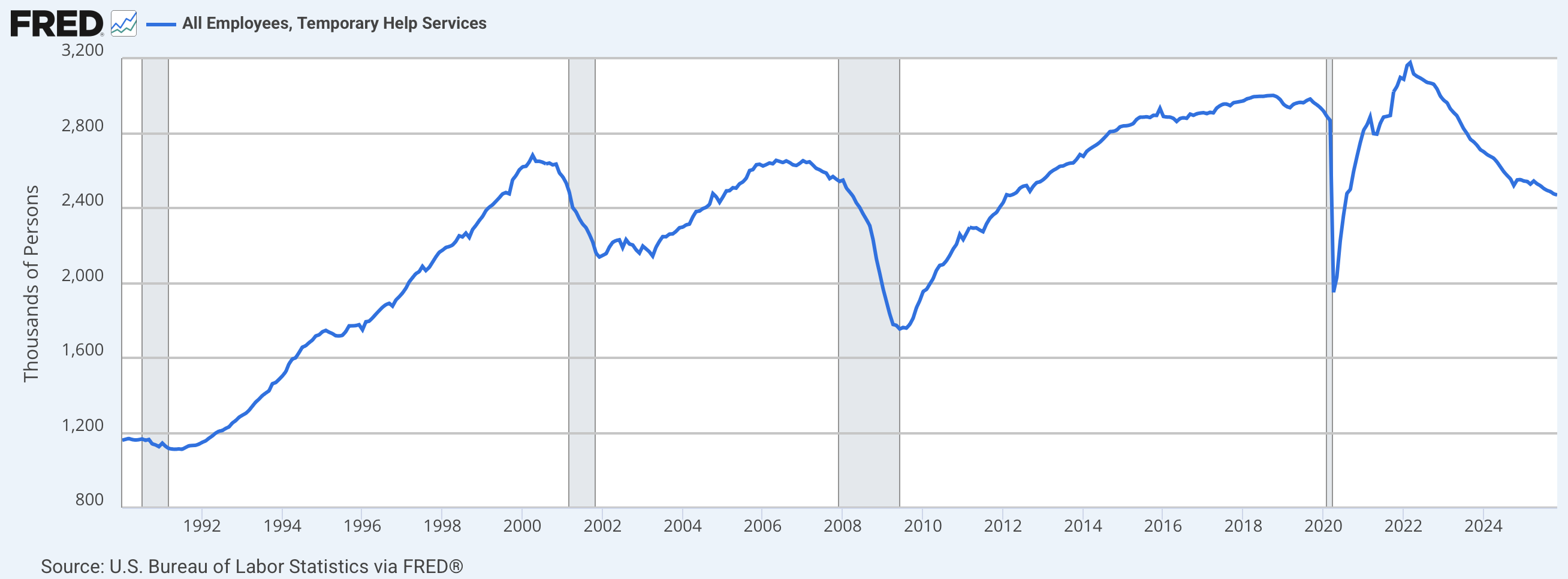

c. Labor Market Cracks: Hiring plans have collapsed to 500k (lowest since 2016). temporary staffing - a classic leading indicator - is seeing its first major drawdown without an official recession; it is likely masked by the gig economy.

4. European Defence: The show will go on

I think markets underprice how structural this is. Don’t get me wrong, it’s not because EU has a real strategy or it became competent all of a sudden, it’s mostly an existential issue for German industry and a real fear from East/Baltic European countries.

- If Ukraine ceasefire happens, these stocks will crash hard in the short term. Those RHM multiples now pricing a forever war.

- However, the spending - especially by Germany, is structural and already committed. I don’t think this is driven by anything else than Germany’s self-interest - to apply Keynesian economics to find some growth since

- a. the 2022 energy shock with Russian gas and

- b. China from the biggest exporter became the biggest competitor killed their whole post WW2 industrial model (autos/ chems) to become the “sick man of Europe” once again. They need to build tanks instead of cars to keep them factories running

- Germany, unlike France or the UK actually has the balance sheet to do this

- The fear in the Baltics and Western Europe for a war with Russia is real (or at least must become real since the mainstream media keeps repeating this) which indicates this is far from over.

- It is interesting to keep an eye on how Russia views this as well:

5. Ukraine Ceasefire - the reverse Nixon

Trump pushes hard for a so-called “Reverse Nixon” strategy to decouple Russia from China. He has already withdrawn the support for Ukraine and is making Europeans pay for it. It is very clear what Trump wants: the war to stop, bring Russia closer, disengage from Europe.

My view is that the main risk against a ceasefire deal is Putin himself as he can wait to gather more gains.

Consider the following points:

a. The recent US security strategy document quite favorable to Russia’s views and very dismissive of Europeans, even to the point of discussing how to undermine them (there are too many crazy excerpts)

b. It proposes the creation of C5 (core 5) - a body like the G7, comprising of US, China, India, Russia & Japan - cutting out the Europeans c. Recent anti-corruption probes and removals of very high ranking officials in Zelenskiy’s government (e.g. Yermak) at the same time the Witkoff 28 plan was discussed (btw Witkoff advised a top Kremlin aide, Yuri Ushakov, on how Vladimir Putin should best pitch a Ukraine peace plan to President Donald Trump) could be related with an effort to remove Z and open the road to a deal with Russia d. 28 peace plan that was floated mentioned quite a few areas of cooperation between Russia and US

6. US-China: A “modus vivendi”

A shift from pure hostility to transnationalism. I do not buy the view that US and China are arch-enemies into a new cold war. I think both are realist states that can project that rhetoric (esp Trump) as a show but behind closed doors they agree on the benefits of trading with each other and keep a calm relationship.

Trump uses rhetoric and threats to actually achieve a deal. The bigger the guy, the bigger the rhetoric and the threats. China never caved, cause it could afford not to. And went on the offense with the Rare Earths chokepoint.

My view is that Trump will trade tariff reductions for massive Chinese purchase commitments to support the US economy.

i. Present that as a big win for the “G2” and himself as the biggest deal breaker. He’ll take the plane and visit Xi in Beijing to do a “deal”.

ii. Midterm elections looming. Trump needs some fiscal stimulus and a deal with China will help with that

iii. On October 25th the RAND Corporation, a semi-official think tank with close ties to the U.S. Defense Department, published a report entitled Stabilizing the U.S.-China Rivalry which was then withdrew which was advocating a more balanced view of China. The 100 page document is noteworthy in that almost a quarter of the report concerns problems with interpreting Chinese intentions

iv. At the same time, the Chinese government released a white paper on arms control and nuclear proliferation. This is the first time in 20 years that the Chinese government has comprehensively stated China’s policy by releasing a white paper, and therefore is a major signal from Beijing. It reveals an extensive effort by China to engage in multilateral arms control initiatives and represents an example of a potential opening for dialogue between the major nuclear powers of the kind mentioned in the now withdrawn RAND report.

7. EU is doomed

I’d like to be more positive on EU but maybe my own biases from the Greek crisis don’t help me. I hope I’m wrong but the continent is doomed.

Europe’s is facing a strategic trilemma:

-

Genuine Autonomy (The Fiscal Impossibility): True independence requires a massive reallocation of capital from social transfers to defense. This implies dismantling the welfare state—a move that is politically toxic and currently impossible to execute.

-

Mercantile Appeasement (The China Trap): A “de-risking” strategy that tries to maintain economic flows with Beijing. This is a short volatility trade—it buys economic time but structurally erodes the continent’s security architecture.

-

US Dependency (Reality): The only viable path. Europe capitulates to reality, accepting total alignment with US foreign policy as the necessary premium for existential survival.

A. Ukraine funding cliff:

- Europe is long rhetoric, short cash & guns. Without the US bid, the EU lacks the balance sheet and the hardware to keep Ukraine afloat.

- All in into the frozen Russian assets as a way out. Don’t hold your breath on that. US is against that and even Japan is refusing to do anything with its own Russian frozen assets. Even France(!) is blocking the release of that €18bn and refusing to disclose bank exposure.

- Belgium is taking the heat publicly but there are serious divides within the EU if this can legally happen and what would be the repercussions

B. The European Union

i. The French Sovereign Crisis: The math just doesn’t work. Debt at 114%, deficits stuck at 6%+, and a revolving door of PMs means zero fiscal discipline. Watch the OAT-Bund spread. If it blows out >150bps, the ECB is forced to step in. This is a Greece-style crisis on steroids.

The ECB cannot let France default. They will have to print (QE) to cap French yields at 4-5%. This is the "pain trade" for Germany—monetizing French debt while Berlin watches its currency debased.

ii. Germany’s Industrial Funeral: This is structural deindustrialization, not a cycle.

a. **Energy Suicide:** Shutting nuclear + expensive LNG to replace cheap Russian gas = the chemical sector is dead. PMIs in contraction for 30+ months.

b. **The Trump Hit:** Tariffs wipe 1.5% off GDP. Germany is staring at a deep recession, which hands the Eastern states to the AfD on a platter.

iii. Demography: The labor force is collapsing.

* What will be the worker-to-retiree ratio by 2035? The welfare state is mathematically insolvent. You can't fix this without permanent 5% GDP cuts, which is political suicide.

iv. Brain Drain: The talent is leaving for the US, UK or Switzerland

v. Political Fragmentation: The center is collapsing. Populism on the rise everywhere.

vi. Migration & Green Deal: Failed migration policies and the ESG/Green Deal stranglehold (plus Mercosur) are fueling the Right (RN, AfD, Vox). The farmers are the leading indicator here (e.g. in Greece today).

vii. Paralysis by regulation: Draghi gave them the roadmap to fix productivity (which is 30-40% below the US), and while everyone agreed, it was mostly agreed. Europe is regulating itself into irrelevance. No AI strategy for example.

viii. Geopolitical Liquidation: The US Put is Gone: Europe caved to Trump because they know the security umbrella is folding. Meeting the 5% NATO target by 2035 is a fantasy for most members.

ix. China is the Bid: While the US leaves, China is buying the distressed assets—ports (Piraeus in Athens, Genoa and Trieste in Italy), infrastructure, and the German Mittelstand - all those failing factories

x. The Veto Trap: If things get hairy, Hungary (or others) can veto everything. The so called “solidarity” will be tested.

8. China Upside

The pivot to “New Three” industries (EVs, Batteries, Renewables) is working. Beijing has “dry powder” for stimulus if growth drops.

- Goldman Sachs forecasts 4.8% growth in 2026, beating consensus.

- China dominates the supply chain for the future economy (80% solar, 60% EVS)

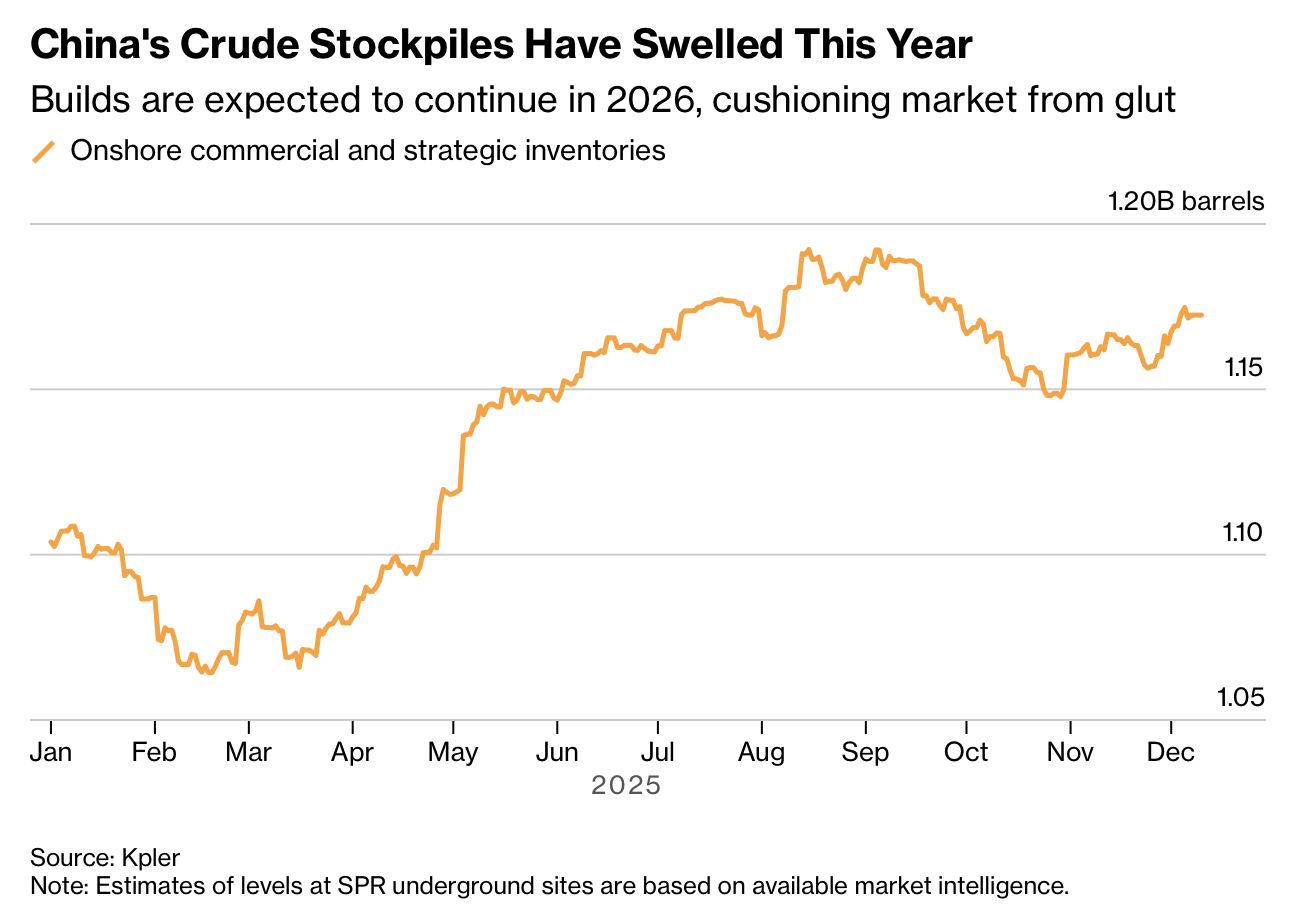

- It has been stockpilling Oil given the cheap prices in unprecedented levels

-

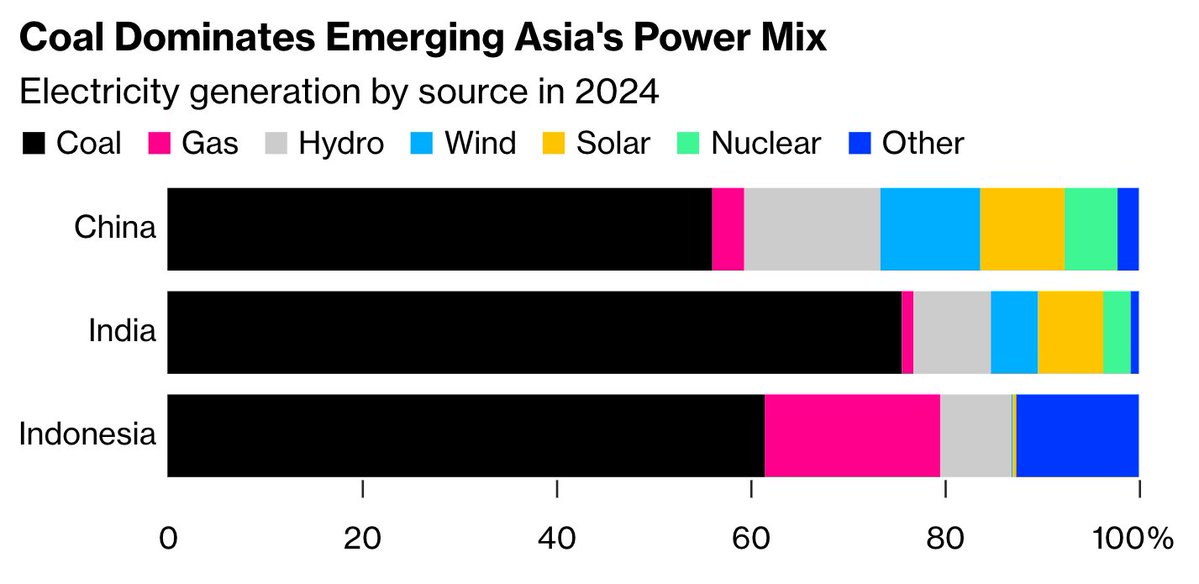

Can use hydro energy when it rains and can switch to pure old coal when it is not. Its “developing nation” status and the lack of any Green Deals helps

-

Is not far from the US in the AI race using human ingenuity (actual), human ingenuity (stealing) and AI talent without the huge capex by the US hyperscalers

9. AI Bubble: Gradually, then suddenly

Knowing that something is a bubble and predicting when it bursts are two very different things. I have no idea about the latter.

I’ll quote Howard Mark’s note from the other day “Is this a bubble?”

One of the most interesting aspects of bubbles is their regularity, not in terms of timing, but rather the progression they follow. Something new and seemingly revolutionary appears and worms its way into people’s minds. It captures their imagination, and the excitement is overwhelming. The early participants enjoy huge gains. Those who merely look on feel incredible envy and regret and – motivated by the fear of continuing to miss out – pile in. They do this without knowledge of what the future will bring or concern about whether the price they’re paying can possibly be expected to produce a reasonable return with a tolerable amount of risk. The end result for investors is inevitably painful in the short to medium term, although it’s possible to end up ahead after enough years have passed.

https://www.oaktreecapital.com/insights/memo/is-it-a-bubble

a. My favorite charts on why this is a bubble:

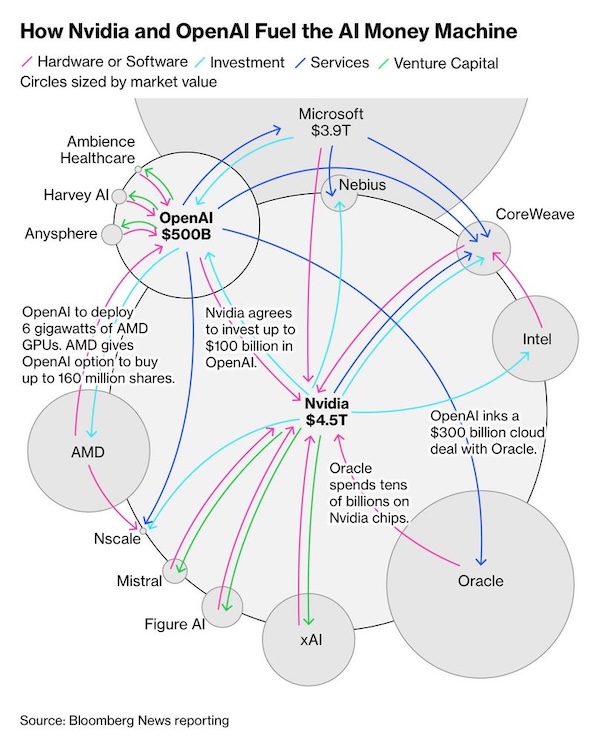

i. The reciprocal transactions containing red flags such as the pre-sold capacity at thin margins (Oracle’s cloud unit earned only about $0.14 in gross profit for every $1 of AI cloud services sold in recent quarters ) and complex financing structures (e.g. xAI’s $12.5 billion off-balance-sheet vehicle to lease NVIDIA chips)

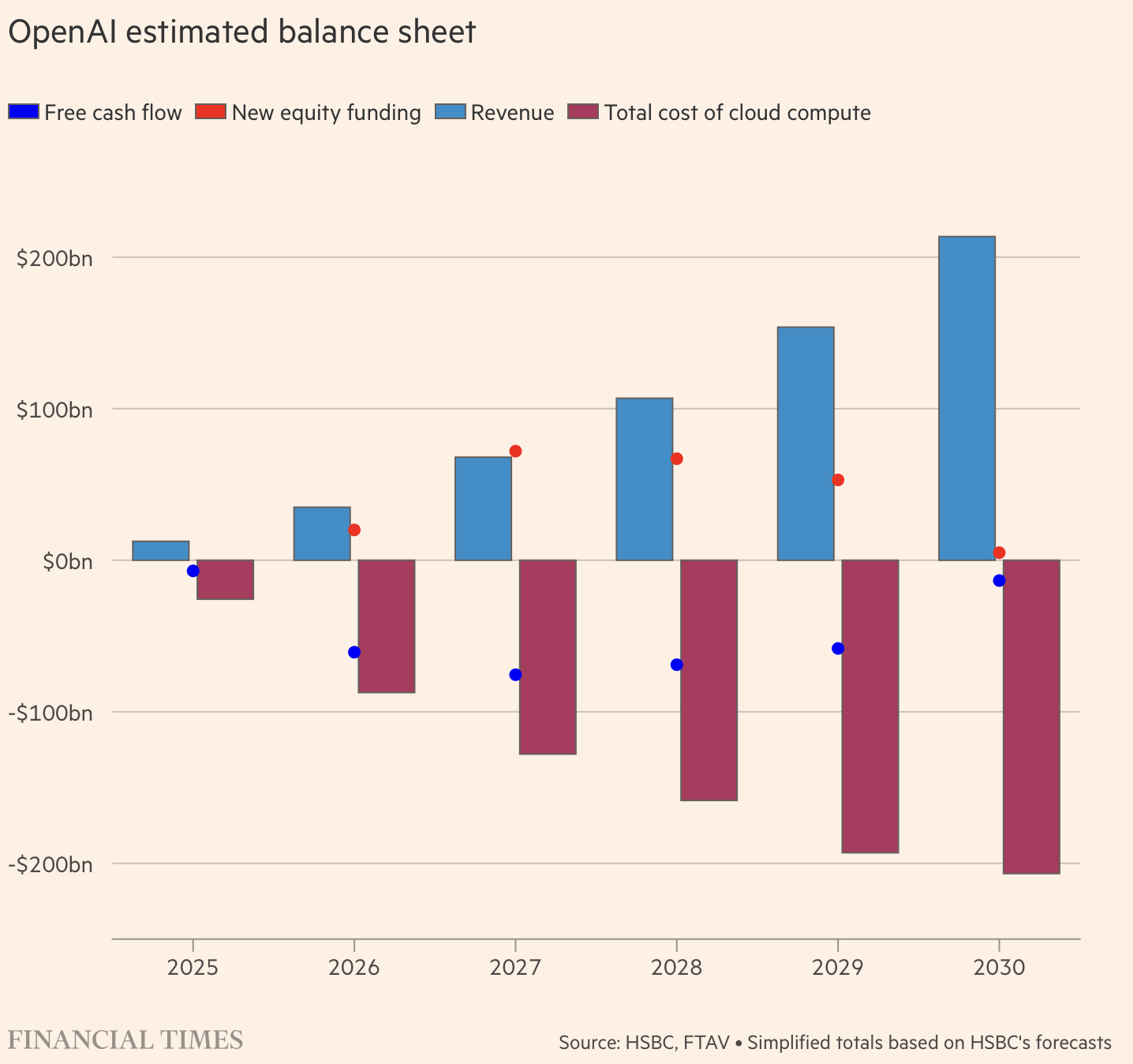

ii. OpenAI, the no1 company and pioneer of the space:

https://www.ft.com/content/23e54a28-6f63-4533-ab96-3756d9c88bad

Generally, I expect a few more iterations of a company releasing “the best” model and leaping ahead of the others. Sam Altman’s code red means they’ll rush to release even half-baked stuff so it can get the PR of being ‘the best’ again

a) IMHO Google will be in the AI winners i) Already has the ecosystem to actually make AI useful, monetizable and the resources to innovate and push the boundaries of R&D ii) Deal with Apple to power iPhones with a custom version of Gemini iii) Already has invested $1bn in Anthropic and is in talks of deepening that investment. Claude has emerged as the winner for code focused AI

b) OpenAI could become what Netscape was for the Internet, the first browser and then it died

c) Could Apple have the last laugh here? They never believed you could achieve adequate ROI on that capex and just focused (without success so far) on how to use AI into their products.

10. Oil Price

The prevailing view (and the most likely) is that oil prices will stay low

-

The consensus is quite bearish (around $60) for oil prices in 2026

-

The Super Glut narrative

The risks on the upside:

-

OPEC+ is focused on building market share but a sustained period of low prices could force the cartel to change course

-

Saudi policy shift and Saudi to stop suppressing prices in 2026 as much as it did in 2025. They need to fund their “Vision 2030” and they can do a lot of borrowing, delay projects etc but they cannot afford to keep prices so low just to help Trump forever.

“According to the International Monetary Fund, the Saudi government needs a breakeven price of around 111 per barrel.”

-

The current underestimation of demand. The oil market is currently facing a crisis of data transparency, with major agencies providing vastly different demand forecasts for 2026. This divergence is creating significant confusion for traders trying to price future contracts.

The Spread: There is a 1.8 million b/d gap between the most bearish and bullish forecasts:

§ IEA (Bearish): 104.7 mn b/d § EIA (Middle): 105.2 mn b/d § OPEC (Bullish): 106.5 mn b/d

The “Missing Barrels” Mystery: Martijn Rats (Morgan Stanley) highlights that the IEA’s model contains 1.13 mn b/d of “unaccounted” oil—barrels produced but not recorded as consumed or stored.

Rats suggests this likely means demand is being underestimated. If demand is actually stronger than reported, it challenges the narrative that the energy transition is rapidly eroding oil consumption.

-

Geopolitics i) A new flare up in Middle East (minimal, even with the last 12 days war between Iran-Israel, oil did not move much) ii) Attacks on Russian oil infrastructure iii) If Trump actually sanctions Russian oil

-

Faster than expected demand i) Global economic stimulus by US and China ii) AI Build out iii) Chinese stock piling

-

Market Positioning: Hedge funds are max bearish so any news or supply shock could trigger a sharp snap higher